Strategic Horizons

Global perspectives from Oaklins, bringing insight into the trends shaping markets across boarders.

Author: Roger Lee, Head of Equity Strategy

In our second edition of the new Strategic Horizons report, we will be looking at why this year’s World Economic Forum may be the most significant conference for years, and - as usual - review some of the major market trends over the last couple of weeks.

I generally don’t care for Davos, not because of the lecturing from the global elites on climate change as they line their private jets up or that they can expense the $75,000 ticket. No, I dislike Davos because I am jealous. Jealous that I can’t spend the most depressing week of the year shmoozing with the great and the good at the most exclusive cocktail party in the world.

But not this year… I think the implications from the 2026 “In the Spirit of Dialogue” World Economic Forum could resonate around Europe for years. Because Team Trump came to Davos and presented the ‘European Establishment’ with a new world order.

How Europe responds could determine not only the survival of the post-war political supranational structures but the economic and political direction of the continent…

A new alternative world view… (well, not that new)

Team Trump was out in force over the week. ‘Bad cop’ US Secretary of Commerce Howard Lutnick seemed to be really spoiling for a fight, and even the more cerebral ‘good cop’ Scott Bessent played his part; both were softening up the WEF before ‘the sheriff’ arrived.

Lutnick kicked it all off at the beginning of the week with excoriating attacks on all that the WEF represents, clearly articulated in the FT in one of the most important op-eds I can recall. And just in case anyone was in any doubt as to why the US delegation was there, his opening paragraph spelt it out:

“We’re not going to Davos to uphold the status quo. We’re going to confront it head-on”.

…and the cowboy metaphors quickly followed. Lagarde apparently walked out of a dinner he was speaking at, and Al Gore heckled, so it would appear he achieved his objective…

It is very clear now that Lutnick, Bessent and Trump (at least during the more lucid parts of his speech) were at Davos to set out their new world economic order. Explicitly challenging the political consensus of the last 30 years, a consensus personified by the WEF. A new economic strategy that they believe will perpetuate US economic and global hegemony.

Their new economic strategy is in fact nothing new. It’s based on as close to an economic truism as you can get and referenced many times in these pages.

Economic growth requires a low tax burden, low regulation, and low energy prices. Economic security requires shorter supply chains and more domestic production, which in the US has been accelerated by tariffs. Through the bluster and bullying that is in essence the ‘new’ US economic doctrine which this US administration is ruthlessly pursuing. And brought to Davos to sell to Europe.

But none of this is new. Had you asked Mrs Thatcher or President Reagan for their views on globalisation, net zero or mass immigration, you would likely have received a similar - if rather more diplomatically phrased - response to the one Secretary Lutnick and Trump have been offering all week.

And the argument is more nuanced than simply an isolationist United States, because Team Trump was also clear that ‘America First is not America alone’. When America wins, the world wins… again, whatever your view of Trump, economically that has always been true.

Team Trump also came to Davos to gloat about how well this economic shock therapy is working… over 4% GDP growth in Q4, and no sign of the tariff induced inflation surge that many, including me, were forecasting. The US economic success story was set out as a clear compare and contrast with Europe.

Now depending on your view of the new administration, this attack on the existing European consensus is a ‘True Danger’ according to Friday’s Economist. On the other hand, perhaps from the perspective of Europe’s populist parties’ perspectives, it’s merely ‘Tough Love’… do it our way and your economies will grow, carry on with these ‘failed policies’ and you won’t.

Scott Bessent perhaps gave the clearest insight into why a change of political direction and higher growth in Europe is so important… “Europeans have focused more on social welfare, healthcare and building schools while the US bears the brunt of defence spending”.

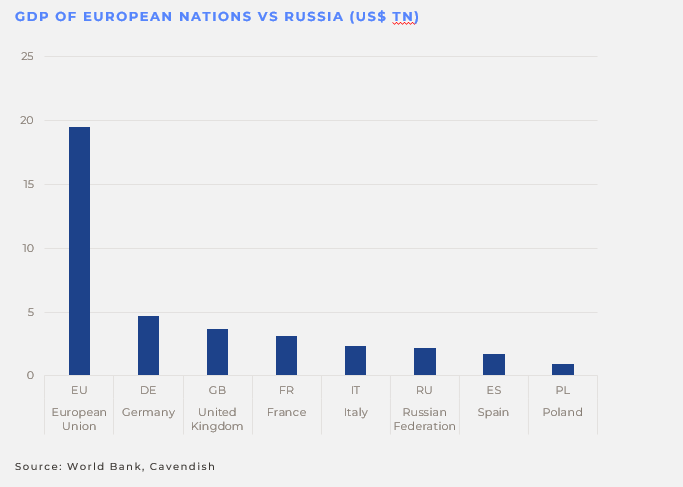

And that’s the key… only through growth and a change in social welfare priorities can Europe spend more on defence and not be as dependent on the US. Europe has 10x the GDP of Russia, so why is it so reliant on the US to defend Ukraine and even its own borders? Why should taxpayers in the Mid-West pay for the defence of Europe and their sons risk their lives? From Team Trump’s perspective, they must continue to defend Europe, because of the political choices Europe continues to make.

And those who think the idea that the United States pressuring Europe into becoming economically strong enough to defend itself is somehow new, need only look at the immediate postwar European history.

In the definitive history of that period, Postwar, Professor Tony Judt argues that it was the US that forced Europe to dismantle its prewar tariff barriers, unleashing the growth that became the postwar economic miracle. It was also the US that insisted and paid for Germany to reindustrialise and be readmitted into Europe. The reason was simple: Washington needed a Europe wealthy enough to pay for its own defence.

Europe faces a similar choice now, and the US is goading them into a decision.

Does Europe persist with existing policy choices, high taxes, high social spending, high energy costs, high regulation - choices which are leading to low growth and therefore unaffordable defence? Or take the US approach? If Europe continues to pursue the former, the Trump administration is clearly running out of patience.

The language and behaviour of Team Trump at Davos was intemperate, but the message was clear…

Greenland, policy volatility, more diversification…

You have no idea the risks faced by members of the commentariat… one day you’re writing your weekly macro piece, the next you’re a diplomatic incident as the Deutsche Bank CEO is explaining your views to the US Treasury Secretary… I did feel quite sorry for my former colleague George Saravelos.

All George had said was that the US needs its largest creditor, Europe, to finance its persistent deficits. As has been widely reported this week, this is America’s one key weakness.

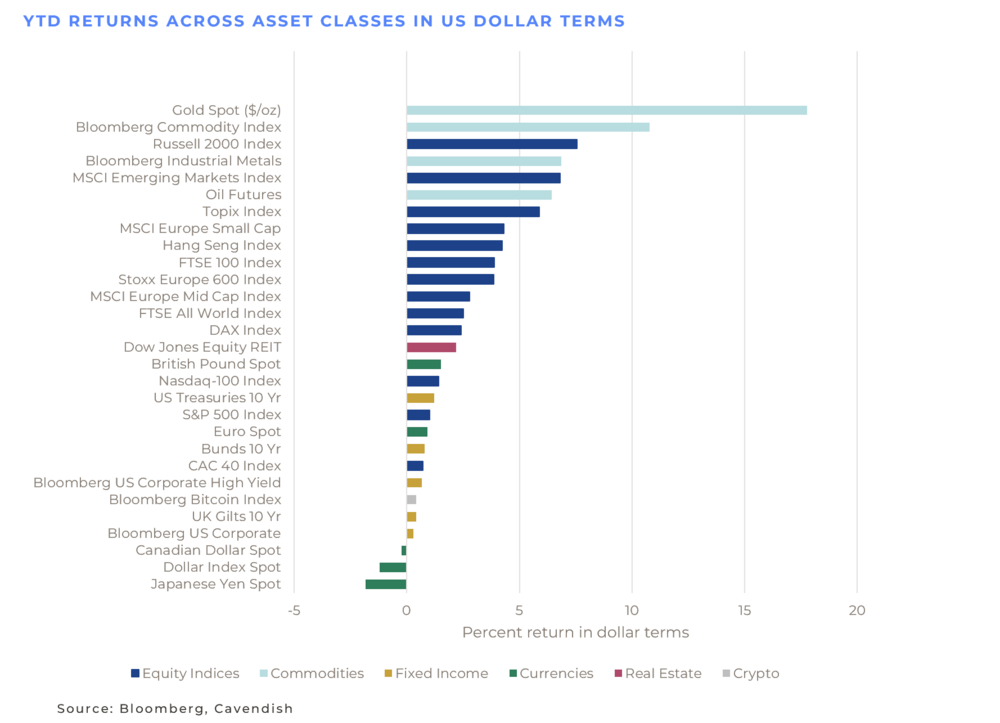

I have no idea if Europe was organised enough to threaten Bessent with a buyer’s strike of US Treasuries or press the nuclear button and follow the Danish pension funds’ lead and sell the lot. But I do agree with George that ‘developments over the last few days have the potential to further encourage dollar rebalancing’ … or, as we have suggested, more diversification from US assets.

I can see no reason why this bullying or goading of Europe won’t continue. Bullies tend not to stop until they are forced to, and so the policy volatility will continue.

A client, in a presentation this week, suggested the market is becoming more desensitised to the policy volatility, which may be the case given the market reaction over the last week was perhaps more muted than previous tariff threats. But as we suggested at the start of the year, owning US assets in the current political environment is far more than owning shares in US companies. Therefore, the diversification trade is likely to continue.

Helpfully, there were headlines that this is happening right now, with PIMCO publicly discussing diversification away from US assets as a direct result of Trump’s “unpredictable” policies. Their CIO Dan Ivascyn (bravely) publicly stated that the $2.2tn fund manager was “diversifying” its portfolios as “we do think we’re in a multi-year period of some diversification away from US assets”.

This was the key dynamic of 2025 and year to date; we would concur that it looks set to continue but just don’t tell Scott Bessent I said so…

AI – winners and losers…

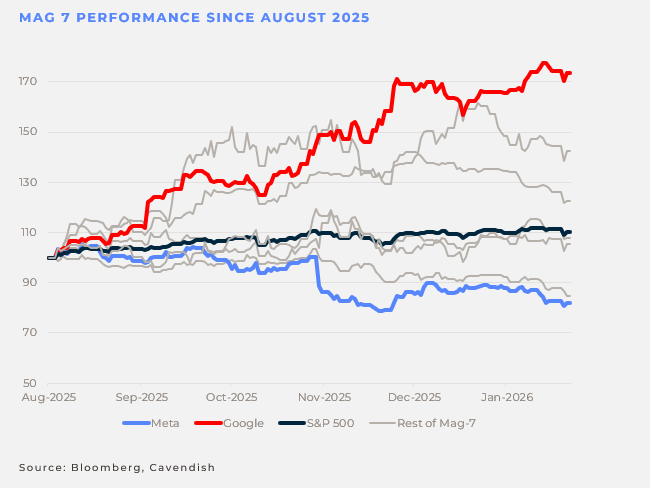

In our (almost) weekly update on AI, there definitely seems to be a consensus forming on who the winners and losers will be in the AI arms race, as we discussed last time. Google with its Gemini chatbot seems to be wearing the maillot jaune. But what about the losers? Amongst the quoted Mag-7, Meta seems to be on the naughty step as can be seen on the chart below…but what about the unquoted sector…?

Big Shorter, Michael Burry, has been vocal again and reposted a very interesting thread from George Noble, a former colleague of Fidelity’s Peter Lynch… who was even more vociferous about ChatGPT and its parent OpenAI, who I see are taking the tin around the Middle East in the latest funding round… so over to Mr Noble, and I would add we haven’t checked any of his assertions…

But according to Mr Noble, OpenAI LOST $12bn in a single quarter according to Microsoft disclosures and Deutsche Bank estimates $143bn in cumulative negative cash flow before the company turns positive; or as their analyst said, “no startup in history has operated with losses on anything approaching this scale.”

And apparently, it’s getting worse, because as Google’s Gemini seems to be eating into ChatGPT usage there’s also been a talent exodus. That is a sure sign, if ever, that there may be trouble brewing…

But Mr Noble also talks about how the AI investment cycle will come to an end and, something we have discussed, where’s the revenue? He even goes further and suggests there are now diminishing returns… and that doesn’t sound good at all…

Sam Altman said last year that investors are “overexcited about AI” … I wonder where that is in his latest pitch book?

Small and Mid-Caps benefit from more diversification…

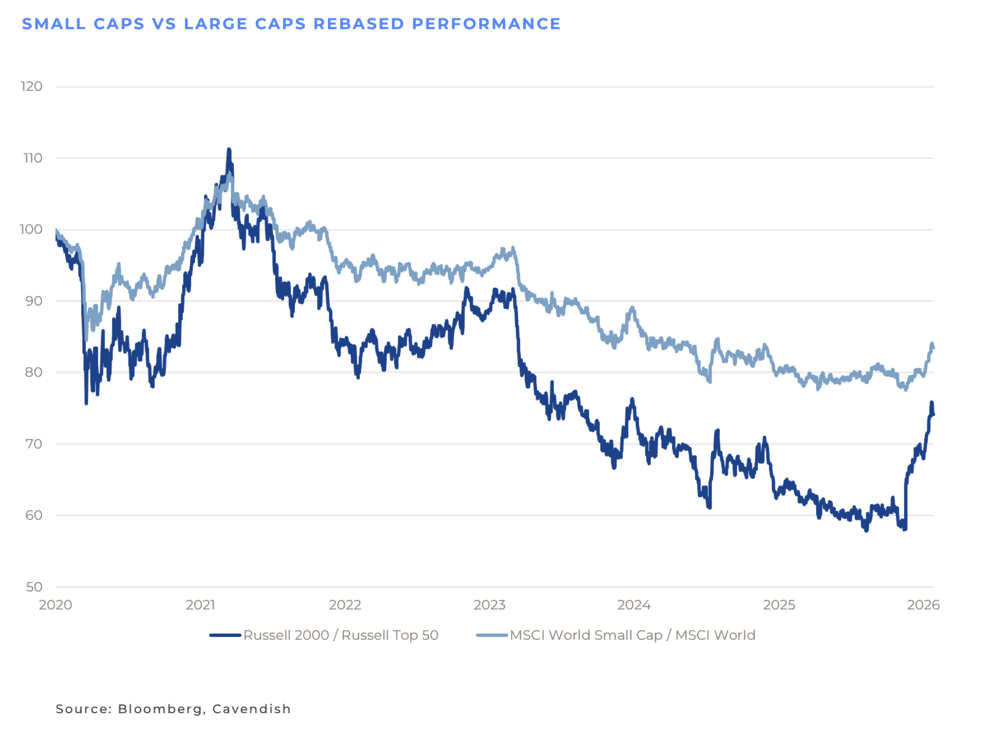

As we also hoped, any diversification would eventually help small and mid-cap stocks. When we have seen these rotations in the past liquidity tends to seek liquidity, hence the relative outperformance of large caps. Eventually the performance starts to broaden out and flow down the market cap into small and mid-cap stocks. That seems to be happening now, with a remarkable start to the year from the Russell 2000, the benchmark SMID index in the US.

The Russell 2000 outperformed US large cap stocks for 14 sessions in a row in 2026, the longest stretch of wins over large caps apparently since 1996… That is the power of diversification when it gets going and given the concentration in Mag-7 and the AI trade, there is potentially a long way to go…

Japanese Government Bonds (JGBs) – the calm returns for now…

Does the level of sovereign debt matter? Most of us in Europe can clearly remember the European sovereign debt crisis and the UK’s gilt crisis in 2022 so the answer is very much yes; but it hasn’t mattered in Japan for the last couple of decades. The Japanese government has had seemingly unlimited capacity to do QE, yield control, fiscal stimulus, whatever it took to try and recover from the deflationary spiral of the last 35 years…but when is enough enough?

Japanese PM Takaichi proposed election and more importantly her planned reduction in consumption taxes are the immediate causes of the recent yield spike, but the problem has been brewing for 35 years.

Japan’s debt-to-GDP is a staggering 235%, and it has the third largest debt market on the planet with $7.4tn outstanding… Yields on 30 yr JGBs have gone from nothing to c. 3.75%, and 10 yr JGBs touched 2.3% last week, the highest since 1999.

It’s hard to see that such a repricing of the third largest sovereign debt market won’t have broader implications and the moves in US Treasuries last week were related.

This repricing of JGBs begs three questions, where the answers might be ‘unfavourable’ to broader markets…

The first question is: if Japan has to pay close to 4% for its 30-year debt, what should the US or European sovereign bonds yield?

The second is more pernicious. At what point will Japanese institutions repatriate their overseas bond holdings to invest in domestic JGBs? Unlike Denmark, Japan is currently the largest foreign holder of US Treasuries with a $1.2tn holding.

And finally, at what point does the infamous carry trade unravel? It’s difficult to quantify how much is in the carry trade – although, to be fair, this re-pricing of JGBs is hardly new news…

The Developed World is more indebted than it’s ever been in peacetime, and the global economy is relatively benign so for the time being the global debt stack is relatively stable. But I hope Mrs Takaichi is very careful because JGBs could bring the whole thing tumbling down…

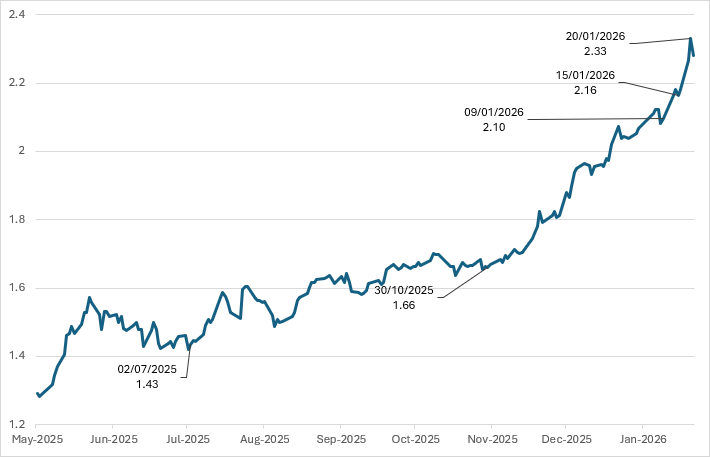

10-YEAR JAPANESE GOVERNMENT BOND (JGB) YIELDS

Things to watch…

As discussed above, how JGBs perform, and the reaction of the Yen will give an indication of whether Japanese investors are repatriating overseas holdings.

The European gas price has spiked over the last week because of cold weather in the US perhaps limiting LNG exports and the cold snap in Europe increasing demand. Higher energy prices, if sustained, won’t be helpful for European industry.

US earnings season gets into full flow with four of the Mag-7 reporting, and a focus on AI incremental revenue generation.

Your contact persons

If you have any questions and would like to discuss the topics mentioned in the context of your company, please contact us. We would be pleased to discuss these matters with you, both in Switzerland and internationally, including broader economic topics and global market developments.

Partner

Kurzprofil

Partner

View profile

Partner

Kurzprofil