Strategic Horizons

Global perspectives from Oaklins, bringing insight into the trends shaping markets across boarders.

Author: Roger Lee, Head of Equity Strategy

I wonder if President Trump is a student of General Carl von Clausewitz or has studied the Great Game, the 19th-century rivalry between the British and Russian empires, because there seem to be so many more dimensions to Operation Epic Fury than just removing Iran’s nuclear and ballistic missile capabilities.

This conflict perhaps needs to be viewed as an extension of Trump’s ‘tariff war’ and the Venezuelan operation. All of these conflicts could be seen in the context of the 21st century Great Game, the rivalry between the USA and China, or as Clausewitz described in his best-known line:

“War is the continuation of policy by other means”.

Once this conflict is viewed through the lens of the struggle for global hegemony between the USA and China, a lot of the questions over how this conflict ends or what happens after fall away.

The easy comparison to the Iraq War is I think confused by the use of ‘regime change’. There are very few similarities in terms of military or strategic objectives. The ‘neocons’ of President George W. Bush had a very different agenda. They genuinely believed in regime change as part of ‘nation building’, where the US could bring democracy to the Middle East, by force if necessary. There lies the contradiction and the reason for the doctrine’s subsequent failure.

I suspect Trump isn’t primarily interested in democratising Iran, although it would be nice if it happened. Other than removing a potential nuclear threat, perhaps Trump is trying to control, directly or indirectly, to whom Iran sells its oil, a similar objective to the Venezuelan operation. Just like Venezuela, China buys virtually all of Iran’s oil at a discount to market prices. Interestingly, one of the few vessels to pass through the Strait of Hormuz this week was a Chinese tanker…

China is the world’s largest importer of oil and needs a staggering 11 million barrels per day. Control China’s oil imports and the US has leverage.

Trump mistakenly thought he could exert economic leverage over China through tariffs, but it transpired fairly quickly that the US consumers’ demand for Chinese dolls outweighed China’s concerns about any short-term economic pain. The possibility of influencing China’s oil supply and making them pay full market price is completely different and so the pivot from tariffs to oil…

The US also solves its secondary problem with China, de-dollarisation. If China is now buying its oil on the open market it will have to settle up in greenbacks, and for that China will ultimately need access to US currency markets.

As Clausewitz argues… war is a political instrument whose object is to disarm the enemy and render him politically helpless… in that context, who has President Trump been fighting this week?

The future of Iran...

Notwithstanding the above, clearly the future of Iran is important, although I would suggest not as important as some commentators make out. Given that anyone who has had any connection with Iran is offering an opinion on its future and likely post-war scenarios, I thought I would offer my insight based on watching two series of the excellent spy thriller Tehran…

There seem to be a range of outcomes emerging; from essentially replacing Khamenei with a ‘son of Khamenei’, which as it happens has literally happened, to an idealised scenario of a Liberal Democratic pro-Western government, with all the options in between, including a Libya-style civil war…

So, there seem to be two ‘worst-case’ outcomes… ‘son of Khamenei’ or civil war.

If the regime does somehow survive while being headed by Mojtaba Khamenei, then is the West any worse off than it was last week? Arguably Iran’s nuclear and ballistic ambitions have been seriously degraded, perhaps even permanently. Iran will still be a global pariah but in this the worst-case scenario, we return to the world we were in last week just with a much-weakened Iran... Every other scenario (from a market perspective if not a humanitarian one) is better than the world we had.

The ‘Venezuelan solution’ of a marginally less malign Iran with a marginally more cooperative leadership, would be a positive for the region and could be the start of Iran’s re-integration into the West. This, I assume, is a satisfactory outcome and anything more pro-Western is a bonus.

Sadly, a Libya-style civil war would be a humanitarian disaster, though perhaps not as bad from a US or Israeli strategic perspective. Libya is no longer a sponsor of international terrorism and sells its oil on the global market.

Commentators can debate about an exit strategy but victory for the US looks like a world where China buys oil from US allies in USD. A victory for Israel is clearer… Iran must never be an existential threat again… As it happens, the outcome could be more positive, because Iran is NOT Iraq.

Sir John Jenkins, a Senior Fellow at the UK ‘think tank’ The Policy Exchange and former UK ambassador to Saudi Arabia and Iraq, wrote one of the best pieces I’ve seen on the subject, attached here, explaining just that. Commentators and politicians are always at risk of fighting the last war.

How long will the conflict last…?

That of course is the unanswerable question. Trump has talked about 4-5 weeks. Other officials have briefed about ‘several months.’

I suspect only two people really know when this conflict will end, President Trump and Prime Minister Netanyahu. What we do know, however, is when it must end – before the US mid-term elections on November 3rd. And so, if it must be resolved by November then maybe we can work back from then to give an idea of the likely timeframe. After all, Trump can’t go into a ‘cost of living’ election with elevated gasoline prices weighing on voters…

As discussed above there is a chance, certainly if there is a ‘positive’ outcome, that the oil price will fall back to pre-conflict levels or even lower, especially if there is a more pro-Western outcome.

But any resolution needs to be reflected at the petrol pumps well before November - and more realistically probably before the start of the summer ‘driving season’. The ‘driving season’ in the US is essentially the summer holidays which typically are taken from Memorial Day, late May, to Labor Day, early September. For pump prices to fully reflect a cessation of the conflict and for supply conditions to normalise, the conflict would likely need to end by early May at the latest.

Which, interestingly, is exactly what the oil futures market is pricing…with prices back down to $70/bl by September.

There are also a couple of arguments why the conflict could end sooner. There are rumblings of discontent not necessarily coming from the leadership of the Gulf States but from ‘sources close to leadership’ that there is a limit to how much collateral damage they are prepared to absorb.

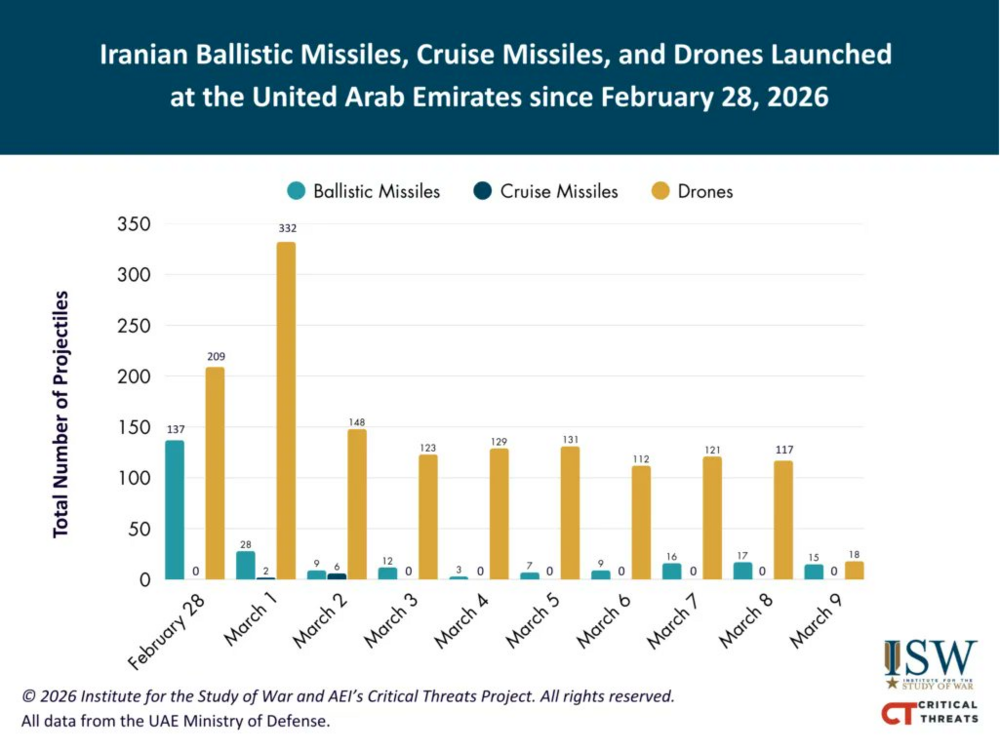

Or perhaps more positively when the US/Israel coalition has degraded Iran’s ability to launch missiles and drones. There is clear evidence to suggest the tempo of Iranian missile strikes has started to subside, the US command talk about a decline of 90% which is a result of US-Israeli strikes on missile launchers (or Iran is conserving their remaining missiles for later in the conflict.) Drone strikes are also falling in their frequency so maybe there is some evidence that the attritional offensive strategy is starting to work. This can be seen in the data published for instance by the Government of the UAE below.

The conflict would be over when one side runs out of munitions. Although there doesn’t seem much evidence that either side has reached that point yet…

Why is the oil price not higher...?

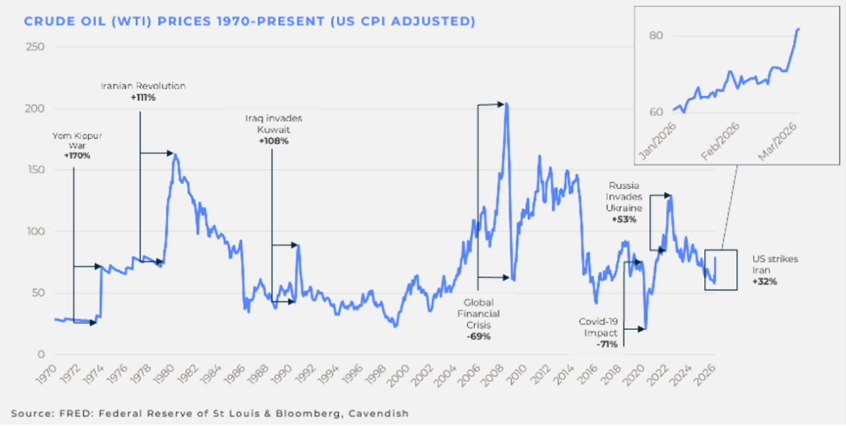

There seems almost to have been a slow-motion reaction from oil markets to the conflict which is surprising and perhaps suggests an optimism that the conflict will be over sooner rather than later. Although Israeli attacks over the weekend on Tehran’s storage facilities seem to have shattered any illusion that oil infrastructure is off limits and the oil price has finally started to respond.

The concern within the oil market was initially that the Strait of Hormuz, through which 20% of global oil flows, was closed. But even then, most analysts forecast oil at least a $125/bl if that were to happen, yet oil is still (at the time of writing) comfortably below that, despite the spike over the weekend. And now the market doesn’t just have to worry about the closure of the Strait but also attacks on the Gulf’s oil infrastructure which has so far been limited.

With c.500 ships waiting to cross the Strait and virtually no vessels moving in and out of the Gulf, the strains on global energy production are now becoming clearer. China and Japan are restricting exports of refined products and Trump is allowing India to import sanctioned Russian oil. Qatar’s energy minister suggested that Gulf exporters could stop shipments within days. …so why isn’t the oil price higher?

I can only think that the market believes Scott Bessent and the US administration are as good as their word and will underwrite insurance while the US Navy provides security, because there is historical precedent for both…

The Strait of Hormuz and the Gulf has been ‘closed’ once before, during the so-called ‘Tanker War’ in the 1980s, part of the larger Iran-Iraq War.

I can only vaguely remember this Tanker War but apparently over 500 commercial vessels were attacked by both sides, partly to restrict their enemy’s crude exports and, from Iran’s perspective, to disrupt Iraq’s Gulf allies. It was during this conflict that Iran used short-range ‘silkworm’ missiles and speed boats to attack tanker traffic. In 1987 Kuwait persuaded the US to reflag Kuwaiti tankers and provide a US Navy escort – the first convoy actually hit a mine.

The Tanker War is largely forgotten except perhaps for the tragedy of the USS Vincennes shooting down an Iranian airliner. A US frigate was damaged but very few tankers were actually sunk and shipping through the Strait of Hormuz was never seriously disrupted, which at least suggests the US has some experience and success in navigating a hostile Arabian Gulf.

The difference back then is the Iranians were perhaps reluctant to engage in all-out conflict with the US, unlike today. In addition, the Iranians didn’t have an almost unlimited supply of drones and perhaps the sheer number of ships whose safety needs guaranteeing.

And of course, it’s not that the Strait of Hormuz is physically closed. It’s effectively closed because insurance companies are unwilling to insure vessels and that has prevented cargo and crude shipments. Although I would think personal safety is something of a deterrent.

So, when Scott Bessent gave assurances that the US will announce measures over the weekend to provide insurance for crude and cargo ships operating around the Gulf the market was also reassured. Again, this isn’t the first time the US has offered ‘war’ insurance.

As far back as World War I the US Treasury created a government insurance program for merchant vessels entering war zones. More recently, after 9/11, the US Government backstopped war risk insurance for shipping and aviation.

So, both measures that Trump proposed have historical precedents; the details will need to be worked out.

I think I first became aware of the strategic importance of the Strait of Hormuz ahead of the Second Gulf War. The only surprise, therefore, is why these measures were not put in place as part of the planning in anticipation of Iran’s likely response… and that is concerning...

Oil, inflation, interest rates…and a massive rotation…

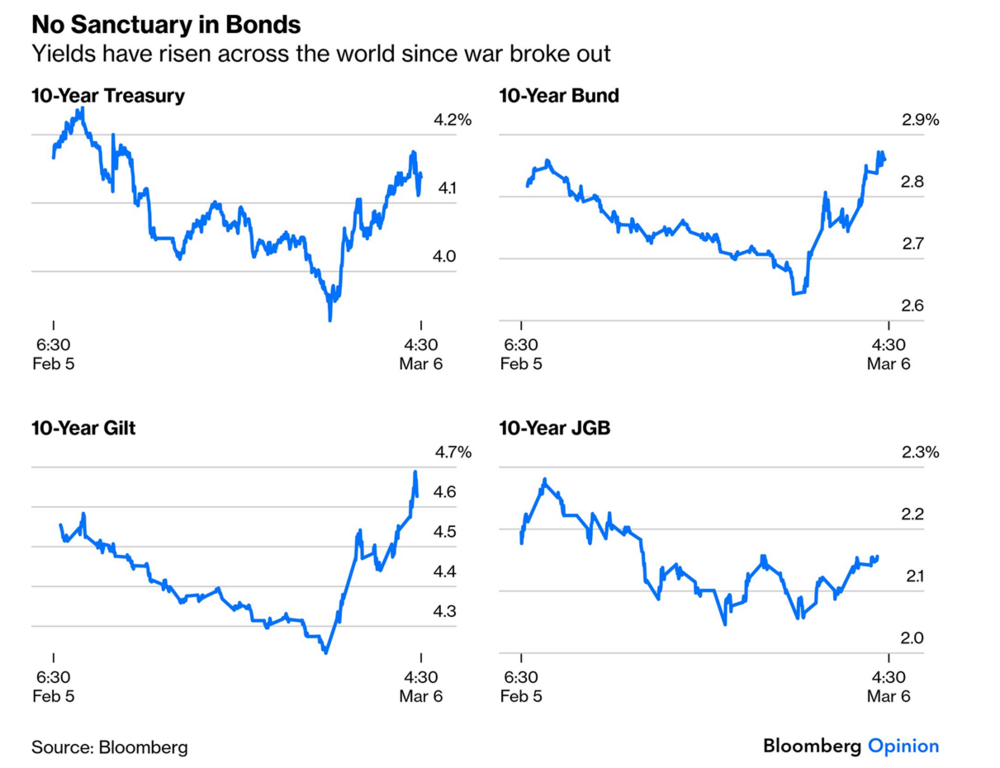

Without diminishing the humanitarian cost of this conflict, from a market perspective the dominant driver of sentiment remains the oil price. The market is following the playbook from the Russian invasion of Ukraine when it probably underestimated the inflationary impact. So given even the recent memory of an oil price spike and the impact that had on inflation, it’s not surprising that the market is extremely sensitive to an oil shock causing a rate shock, and everything then becomes correlated to oil.

The UK and Europe are the most sensitive to an oil shock because of our energy dependency. This is clearly seen in the moves in European sovereign debt, especially UK gilts, which have in turn primarily been driven by an increase in inflation expectations.

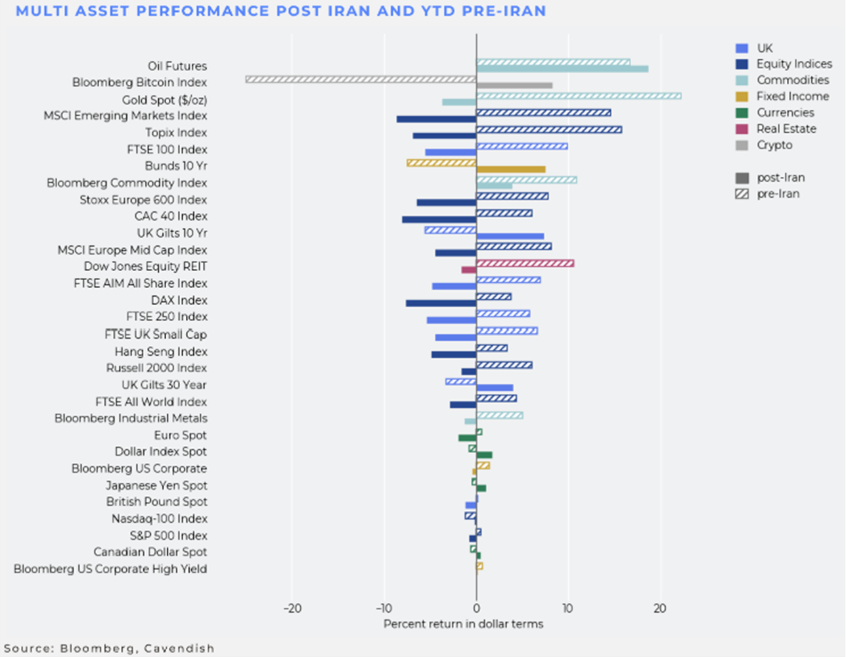

The broader market moves are also reflective of this perceived higher oil-price/interest rate environment. Cyclicality/value has effectively been sold as the market takes refuge in quality/growth. The reverse of what we have seen year to date. The clearest example of this is the relative outperformance of the NASDAQ as mega-cap tech is seen as resilient to higher rates rather than exposed to AI capex risk. The reversal of the year’s winners and losers is very clear across asset classes as can be seen on the chart below. Anything that performed badly at the start of the year has recovered and vice versa.

The risks of a supply disruption are at least in the short-term growing as discussed above. Economic disruption is central to Iran’s strategy. The ongoing risk of disruptions to oil and LNG supplies is increasingly influencing both inflation and interest rate expectations in Europe and globally.

If the US is to achieve its strategic objectives and not succumb to economic pressures, it has to keep the Gulf open. How the US manages its response to these supply challenges is now as economically significant as the way it conducts the broader military conflict.

Things to watch…

Your contact persons

If you have any questions and would like to discuss the topics mentioned in the context of your company, please contact us. We would be pleased to discuss these matters with you, both in Switzerland and internationally, including broader economic topics and global market developments.

Partner

Kurzprofil

Partner

View profile

Partner

Kurzprofil