Strategic Horizons

Global perspectives from Oaklins, bringing insight into the trends shaping markets across boarders.

Author: Roger Lee, Head of Equity Strategy

American foreign policy has long been framed through presidential “doctrines”, a convention that was established by President Monroe and his eponymous doctrine in the 1820s, although many of the subsequent ‘doctrines’ seemed to have been remarkably similar.

The Truman Doctrine—built on the idea of containing communism by providing military and economic support to anti-communist governments and movements—defined the characteristics for subsequent U.S. foreign policy. Its core logic was echoed in the Eisenhower Doctrine, which extended similar commitments to the Middle East, and later in the Reagan Doctrine of the 1980s, which went further by actively aiding anti-Soviet insurgencies. These ‘doctrines’ also explain America’s tragic entanglements in Southeast Asia, where the fear of communist expansion drove increasingly costly interventions.

Yet despite their controversies and human costs, these postwar doctrines collectively contributed to the eventual weakening and collapse of global communism, and the conclusion of the Cold War.

The George W. Bush–era “neoconservative” doctrine of regime change proved far less effective, to the point that the very concept of regime change became largely unwelcome in U.S. foreign policy debates until this year’s Iranian conflict.

So, I wonder how history will describe the current Trump foreign policy doctrine?

I have been fascinated to learn over the course of the Iranian Conflict that Trump first started discussing the threat of Iran controlling the Strait of Hormuz back in the late 1980s. And if it is true that our political views are formed in our 30s then seeing the US humiliation during the Iran hostage crisis and oil shocks of the 1970s suggests there is a leitmotif running through his thinking both in terms of US energy self-sufficiency, ‘drill baby drill’, etc and the current conflagration.

However, if that is the case, why are there persistent inconsistencies? If Trump himself was fully aware of the strategic value of the Strait back in the 1980s why was there seemingly no adequate planning for its re-opening? If Trump recognised the value of seizing Kharg Island 40 years ago why are the Marines still en route a month into the conflict? Even this weekend we had the most extraordinarily contradictory posts...

On Friday night Trump posted comments about ‘winding down our great Military efforts’, and suggested handing over clearing the Strait to ‘other Nations’… so perhaps an effort to ‘de-escalate’ the conflict. Yet only hours later he issued his most bellicose threats so far, expanding the conflict to include Iran’s power infrastructure, with the inevitable Iranian retaliation...

Perhaps this is closer to the Nixon “Madman” Doctrine, the carefully cultivated perceived irrationality of Nixon was in itself a threat.

Given Trump’s latest more conciliatory posts it is not clear how this conflict will end. Maybe negotiation is more likely today than the US Navy clearing the Strait or a military occupation of Iran’s oil terminals, but the way this conflict concludes will determine how history defines the Trump Doctrine, unless - like Churchill - he intends on writing his own history, but in a series of posts on Truth Social.

Foreign Policy by tweet…

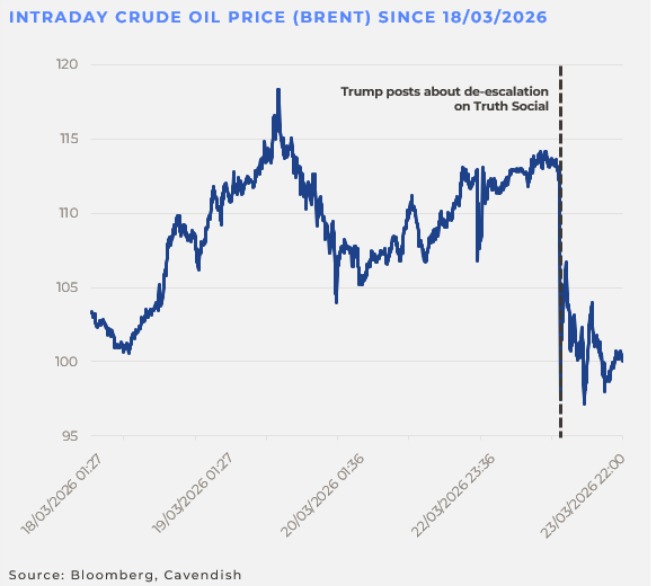

What I am about to write may not age well given the rapid news cycle. But even within the extraordinary market moves we have seen on the back of Trump’s social media posts since his election, Monday 23rd March must rank amongst the 18 most impactful words in market history, “very good and productive conversations regarding a complete and total resolution of our hostilities in the Middle East” and he went on to delay the strikes on Iran’s power infrastructure for five days – coincidentally the deadline is after the market closes on Friday.

Iran state media and the reported lead Iranian negotiator Mohammad Baghar Ghalibaf, denied that talks were taking place, but they would, wouldn’t they? Interestingly on Monday, there were reports of an Iranian Government jet flying to Islamabad where negotiations are supposedly taking place as the aircraft needed a guarantee of safe passage from the US and IAF… There are even suggestions of a 15-point peace plan and that Vice President JD Vance is going to lead negotiations… so who knows...

Did the Iranians really approach Trump? Or are markets, and especially US Treasury yields, the ‘guard rail’ just as they were after Liberation Day and suggestions that 4.5% on the US 10 yr Treasury is the ‘magic number’? Although I can understand why both sides want some sort of acceptable peace.

My knowledge of Iran is solely based on the excellent Tehran TV drama, but it seemed likely at some point following the strikes on the Iranian leadership that someone would emerge who would prefer to maintain their current opulent lifestyle. Venezuela also suggests Trump is more than happy to ignore a leader’s past if they are compliant with the US.

So maybe both sides are ready for an ‘off ramp’, but the key will be how to sell this as a ‘victory’ to their domestic audience. I suspect Iran’s survival for just a month could be sold as a ‘victory’ and a ‘hard man’ from the IRGC, who fought for 8 years in the Iran-Iraq war, would seem to have the sort of credentials to satisfy his own hardliners.

Trump needs to come away with the Strait of Hormuz very much open. The rest is all part of the negotiation, and as Trump said on Monday, ‘he’s been making deals all his life’… so how that ‘deal’ looks and how compliant Iran will be to the US remains to be seen...

But with more US ground troops on the way to the Gulf, it’s also understandable why markets tempered their enthusiasm.

Rate markets react...

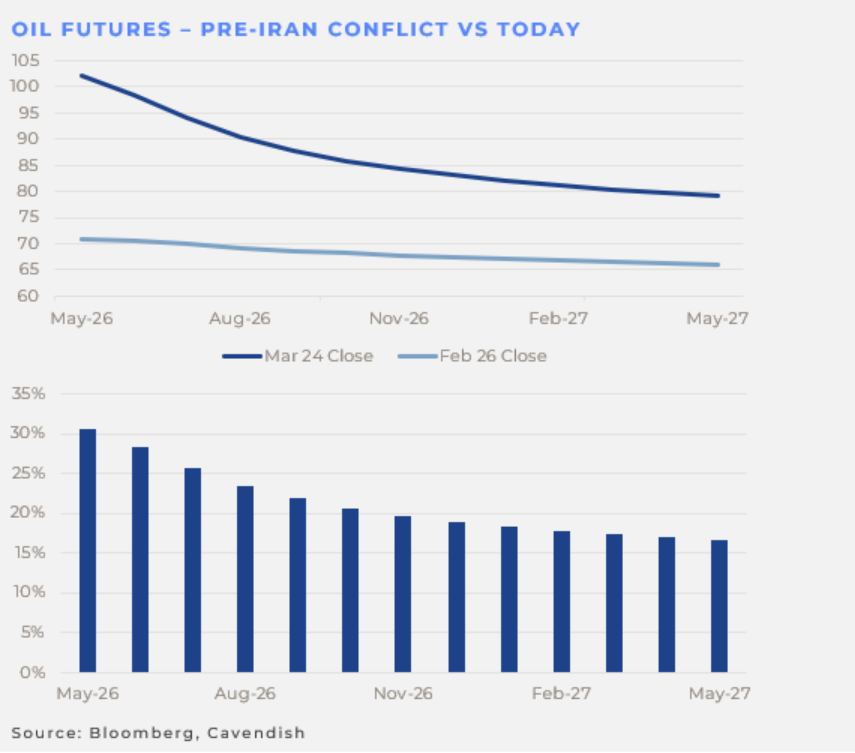

Throughout the conflict there has been plenty of ‘hope’ in the oil market and the oil futures curve has consistently suggested that the conflict will be relatively short. So far, even the spot price has peaked at ‘only’ just short of $120/bl. If you had foreseen at the start of the crisis that the Strait of Hormuz would be effectively closed and that the IEA would describe this as the ‘greatest threat to global energy in history’ then an oil price closer to $150 may not be unreasonable… but so far the oil market has been relatively calm... which is not the case for interest rate expectations.

The transmission mechanism from higher oil prices to inflation is well established, but most economists would argue that it’s the ‘duration’ of higher oil prices that will be the key to inflation and therefore any policy response. And it is generally accepted that a spike in oil prices for less than 3 months doesn’t have a lingering impact on inflation... but that is certainly not what the rates markets across the developed world are pricing in...

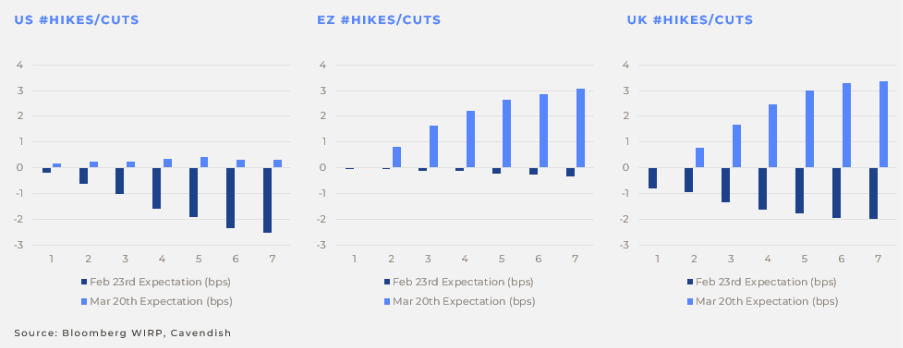

The major interest rate markets seem to have shifted depending on the interpretation of last week’s divergent Central Bank meetings... so, in a very broad summary:

The Fed appears to be the least concerned about the oil shock and given US energy self-sufficiency perhaps has the least to be concerned about. WTI - oil for settlement in Cushing, Oklahoma - is at its largest discount to seaborne Brent in 4 years. The oil price rise is seen as a ‘risk’ to the ‘base case’, but the base case remains that inflation is gradually coming down.

The ECB were more concerned, whilst acknowledging that monetary policy can’t control the price of oil, monetary policy may have to adjust if businesses raise prices, and higher wages are the result. The ECB is treating the oil spike as an inflationary risk but in a current low inflationary environment.

Here the contrast with the UK’s Bank of England becomes very clear and perhaps explains why the BoE was the most hawkish of the Central Banks. Because the UK already has a perceived inflation problem; at least according to some members of the decision-making Monetary Policy Committee. And so, the risks to inflation when inflation is still elevated are more immediate. The UK also had the most scope to cut rates prior to the crisis. So, a combination of reversing positions, and the BoE’s more hawkish tone, means a more extreme reaction in the rates market is understandable.

However, three rate rises in the UK and the Eurozone (albeit from a lot lower base) and almost unchanged rates in the US, suggests different interpretations of the same oil futures curve. I doubt all three can be right...

We keep coming back to the same critical question when trying to interpret where markets are and where they are likely to go… How long is the oil disruption likely to last? At least from a market perception, it is all about ‘duration’.

Government Bonds follow rate expectations

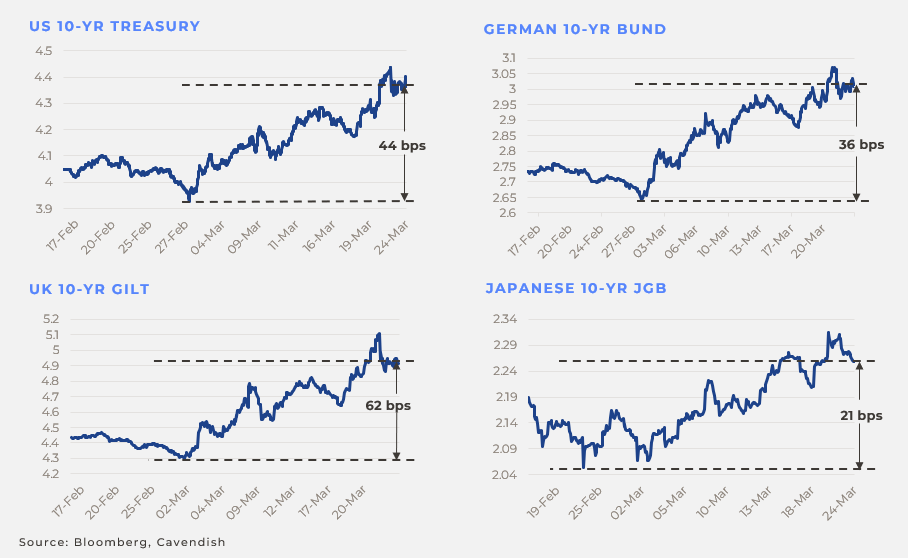

The concept of duration is very familiar to the bond market but not as important now as interest rate expectations. At one level, it is perhaps intuitive to see how the government bond markets have reacted by essentially following the rates market as can be seen below.

What is also striking is by how much UK gilts have underperformed and whilst we are conscious of not being UK centric, I do think the specific issues facing the UK are relevant. Not least because of the risks that an issue in UK Gilts could spread into other government debt markets, as we saw during the European Sovereign debt crisis. This was extensively covered in a webinar last week from around the 33-minute mark, which is attached here.

The UK’s fiscal issues aren’t atypical for a European economy. Growth has been a struggle and since Covid the debt pile has increased to around 100% of GDP.

The new Labour administration has raised c. £70bn in taxes in their first two budgets and the UK has its largest tax burden as a percentage of GDP since WW2, so there is perhaps limited scope to see how taxes can go up further. Yet the government is still spending more than the income it is generating and there is no political will to curb welfare spending, so the budget deficit is stubbornly high at c. 4% (cf France c. 5.5%).

The problems don’t end there. Net Zero policies have created the highest energy prices in the Developed World which is impacting what’s left of the UK’s manufacturing base, yet the economy is still very exposed to energy shocks.

Inflation rose last summer in contrast to Europe primarily because of pass through of government policy, so UK inflation remains at around 3% (cf Eurozone c. 2%) and as a result interest rates are far higher than Europe at 3.75%.

Then there is the political risk of a change in leadership to the ruling Labour Party following a very disappointing by-election and a possible wipeout in the municipal elections in May. The most likely leadership contender seemed to launch her campaign last week with a clear suggestion that the ‘bond markets don’t understand’ her spending plans !?!… And as discussed above, the Bank of England is still very concerned about inflation.

Taking all that together, along with the muscle memory of Liz Truss’ gilts crisis in 2022, and I think it’s easy to see why the bond market is nervous of the UK...

The choice for markets going forward...

Someday this war’s going to end... and that end may be sooner rather than later depending on Trump’s mood… so what sectors and styles will lead after this oil shock?

Will the dominant macro drivers prior to the Iran conflict re-assert themselves? Those two forces driving a re-appraisal of owning the US; policy volatility and AI risk.

Once the conflict concludes, will anxieties have eased over this administration’s policy volatility —or only intensified?

I was on a podcast last week and one of the hosts suggested that this Iran War may be ‘peak Trump’ and what more can he do?

My riposte was that this is a disruptive Presidency, rightly or wrongly, and I can’t see how that disruption ends with two more years to run. And even in the unlikely event Trump is so chastened by Iran that he decides to follow the so-called international rules-based system, isn’t the genie out of the bottle?

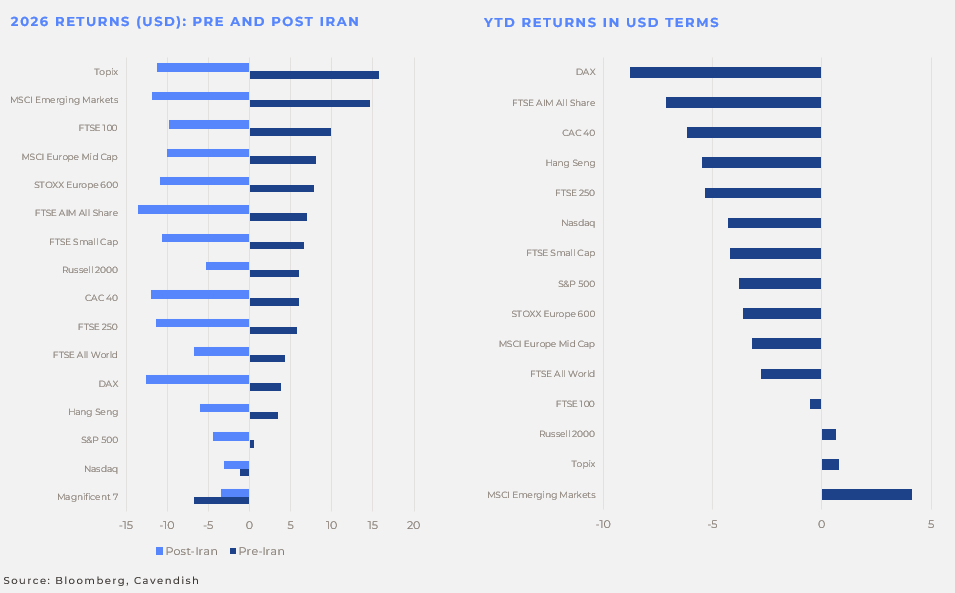

The benefits of diversification were ignored for years when US exceptionalism was in the ascendency. Having only just relearnt the power of diversification it would be surprising if those trends didn’t return and continue after the conflict.

Contrary to market expectations, if the conflict ends soon, it is possible to see how the pre-war interest rate trends reassert themselves. Central Bankers will be relieved that the oil spike has passed with limited second order inflationary effects but instead should be concerned about any lingering economic scarring... This was very much the case after the invasion of Kuwait when the Fed cut rates five times.

And as for the oil price, again this is a clear reminder of the need to ensure security of supply outside the Middle East. There has been a ramping up of non-Middle Eastern oil production which is unlikely to go away once the Gulf states re-start full production. And any sort of positive resolution that includes a more US compliant Iran could mean an oil price lower than pre-war levels.

The monetisation risks around AI certainly haven’t gone away which should continue to pressure the Mag 7, despite their obvious ‘defensive’ characteristics during the conflict.

So, all in all, and this may be rose tinted, but there are good reasons why the trends seen before the conflict will reassert themselves, and if anything could be even stronger for the reasons above. But as ever it comes back to duration... and that seems to be totally up to Trump... which is where the policy volatility came from in the first place...

Things to watch...

At the risk of stating the obvious... the only factor that matters in markets right now is what Trump is thinking... and the only window on that is his Truth Social account… perhaps that is the new foreign policy doctrine... think it; post it...

Roger Lee

Head of Equity Strategy

*This commentary is provided for information purposes only. It does not constitute investment advice or a recommendation. For professional clients only. Views as at the date of publication. No reliance should be placed on this material; onward distribution is the responsibility of the recipient.

Your contact persons

If you have any questions and would like to discuss the topics mentioned in the context of your company, please contact us. We would be pleased to discuss these matters with you, both in Switzerland and internationally, including broader economic topics and global market developments.

Partner

Kurzprofil

Partner

View profile

Partner

Kurzprofil