Strategic Horizons

Global perspectives from Oaklins, bringing insight into the trends shaping markets across boarders.

Author: Roger Lee, Head of Equity Strategy

‘I am Trump, not Rex’ could be President Trump’s election slogan if, as he threatens, he runs again in 2028 and like Julius Caesar, he needs to overcome a bit of a ‘No Kings’ movement. I do wonder if President Trump secretly sees himself as the great Roman general and imperator when he plans victory parades and triumphal arches in Washington.

Iran may also have underestimated Trump’s classical education, because it seems he too has read De Bello Gallico and particularly Book VII, describing Caesar’s defeat of Gaul’s chieftain Vercingetorix (later of Asterix fame…) at the Battle of Alesia.

To besiege Vercingetorix in Alesia, Caesar built one wall around the town, but to protect against an attack to his rear from the other Gallic tribes, Caesar built another wall… in effect a siege upon a siege, and a stroke of tactical genius that saw the defeat and slavery of Vercingetorix and the conquering of Gaul. After this stunning military success, Caesar of course returned in triumph to Rome, crossed the Rubicon with his legions, and the rest, as they say…

There have been many examples of maritime sieges or blockades in history, but I am not sure if there has ever been a blockade on a blockade in such a localised area, and $1tn worth of AI investment couldn’t find one either.

The aim of the blockade is clearly to put economic pressure on Iran without the resumption of bombing or what seems to be called nowadays a ‘kinetic war’. At least according to Trump, the blockade is working, and Iran is being more compliant. It’s not totally clear the Iranians have got the memo given the weekend’s negotiations were abandoned.

However, the US is probably also projecting another important ‘hard power’ message with this blockade. It was suggested at the start of the conflict that exerting control over China’s oil supplies would be a valuable byproduct of a more ‘normalised’ Iran but this blockade also serves as a timely reminder to China that the US can just as easily blockade the Strait of Malacca or the South China Sea ,and significantly impede China’s essential imports… as the British imperialists knew only too well, if you control the world’s seas, you control the world’s trade.

It looks, hopefully and at least according to Trump, that we are heading towards the denouement of the conflict. President Trump, like Caesar, is also prone to exaggeration and hubris. So, it is easy to imagine “victory” being celebrated with the spectacle of a triumphal parade through D.C. And like Caesar’s four-day triumph through Rome, perhaps there would need to be an auriga, leaning into Trump’s ear from time to time to whisper … you are not a god…

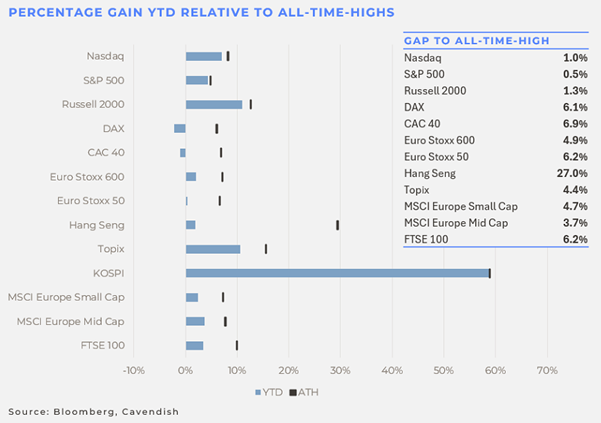

All-time highs abound…

If you are sitting in the US, and you don’t go and fill up your SUV, you may be wondering what all the fuss is about in I-ran… the S&P hit all-time highs again this week crossing 7,100… yet the oil price is still well over $100/bbl and the Strait of Hormuz is very much closed… Even Central Bankers have spotted this anomaly, with the Bank of England’s Head of Financial Stability saying “There’s a lot of risk out there and yet asset prices are at all-time highs. We expect there will be an adjustment at some point.” The Bank of England has a point because European markets aren’t far behind the US.

So, what explanations are there to support the strength of asset prices given the abundance of risk…

We discussed this apparent anomaly a couple of weeks ago and there are also some novel explanations. As it happens, this divergence between the apparent reality and US equities especially was also the theme of a CNBC interview I did last week, so may be worth re-visiting again.

I think the strength of the equity market comes down to a positive, the lack of a negative, semiconductors and, as ever, Trump.

The positive is that there is still a ceasefire and the fighting has stopped. The Strait is closed but it seems that the Fed, at least, is a lot more comfortable with elevated oil prices than the ECB and especially the BoE.

More specifically, the new Fed Chair nominee, Kevin Warsh, thinks that more attention should be paid to the ‘trimmed mean’ inflation, which is certainly helpful during an oil spike. So, from an interest rate perspective, there isn’t that much to see in the US. The US market seems less concerned about the AI threat than before, at least until last night, and the semiconductor manufacturers have especially helped propel the S&P and NDX higher. That, of course, can change (see below).

But there is also the removal of the main negative, a re-start of the so-called ‘kinetic war’ together with the significant increase in risk to the Gulf’s energy infrastructure.

Trump has twice stepped back from a further escalation so it’s not unreasonable to suspect he doesn’t want a return to full-scale fighting. Trump may be happy with a blockade on a blockade if the US stock market continues to rise. The blockade itself seems enough to keep Iran interested in a deal even if it’s not clear with whom the US is negotiating.

The concern must be how long this stasis can last before we run out of the other oil derivative products that people talk about, from fertiliser to helium for chips. Most commodity analysts struggle to understand why the oil price isn’t higher, let alone the other oil products. But the US equity market and that other tech-heavy index Korea’s KOSPI have no concerns…

There is probably a final reason for the market’s resilience in the face of the obvious risks, and what most of us want, emotionally at least. The market still believes Trump when he says the conflict is close to an end and there will be a great deal. Many investors I suspect can’t envisage a long, drawn-out conflict so we want to believe, and on that basis the buy-the-dip makes sense… the only problem with that is Trump has been saying a deal is close since the beginning of March…

Semis lead the AI charge…

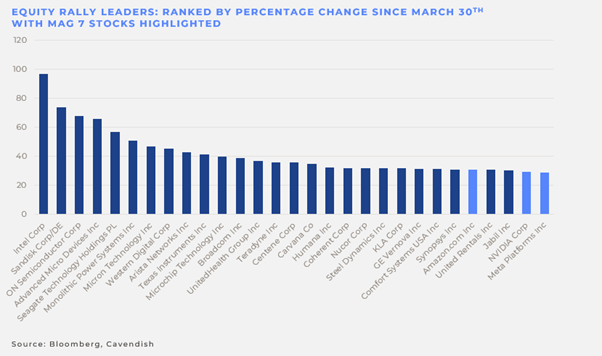

The strength of the US semiconductor index has been truly historic. The Philadelphia Stock Exchange Semiconductor Index (SOX) has risen 47% over the last 18 trading days to the end of last week, as the market anticipates the ongoing capex from the roll out of AI data centres. The SOX advanced every day over that period, the longest rising streak in its history.

The market is definitely taking the view that the semiconductor manufacturers are the clear winners form the AI race, but despite the overall rise of the S&P and NDX discussed above, underneath the surface the market is being somewhat more discerning about the AI implications.

As Robert Armstrong pointed out in the FT’s ‘Unhedged’, whilst the points added to the S&P come from the Mag-7, the relative outperformers are all semiconductor manufacturers since the market bottomed on 30 March. The Mag-7 has performed well but has been less exceptional.

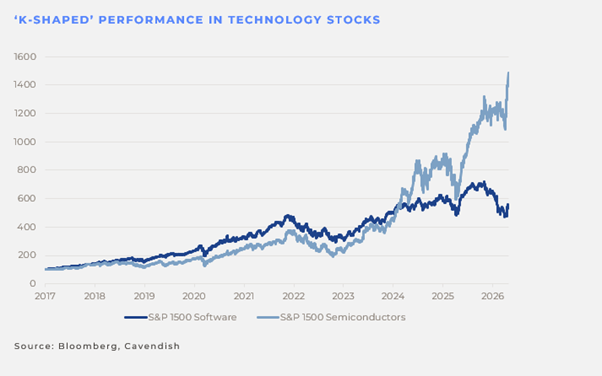

And, as can also be seen on the chart below, the market is still pretty convinced as we discussed last time that the software or SaaS stocks are going to be the losers.

The market is taking a totally realistic and sensible view. Happy to reward the companies that are benefiting from the AI rollout today, but are still being more circumspect about those companies like the so-called hyper-scalers that are paying for the AI build-out. And the market has come to a very clear conclusion about who is going to lose.

It may be hard to justify a 47% rally in 18 trading days, but the logic is at least understandable.

Is the UK ungovernable…?

The UK may be about to replace its latest Prime Minister after only 20 months in office and a historic election win in July 2024 ….

I am not sure how much coverage the UK’s latest scandal has generated globally but at least it’s not about a birthday cake, unlike Boris Johnson’s resignation. It centres around the appointment of Labour grandee, Peter Mandelson, one of the key figures behind Labour’s resurgence under Tony Blair and a former EU Commissioner, as Ambassador to the United States.

The risks were also clear: Mandelson was a known acquaintance of Jeffrey Epstein, had had to resign twice from the UK Government and had a consultancy business with close relationships to Chinese and Russian companies… but other than that (?!?), it was an appointment that UK PM, Sir Keir Starmer, considered worth the risk….

Perhaps inevitably, as more revelations around Epstein were published last September, Mandelson was sacked as US Ambassador. However, the attention then started to focus on how the original decision was made and this came to a head two weeks ago in a newspaper scoop that Mandelson was appointed despite failing a security vetting.

The PM - somewhat as a reflex reaction - sacked the most senior civil servant at the Foreign Office, but in justifying this decision and explaining the appointment to Parliament the PM made some claims that are now being challenged by the Opposition and seem to contradict evidence from the civil servants involved. In the UK it is customary that if a minister, including the Prime Minister, has misled Parliament they should resign. And with more than a touch of irony, this is the same standard that Starmer held PM Boris Johnson to when he was in office…

Overlaying this scandal onto the municipal elections in the UK where Labour could come fifth and suffer their worst election result in the history of the party, the political pressure on PM Starmer is immense.

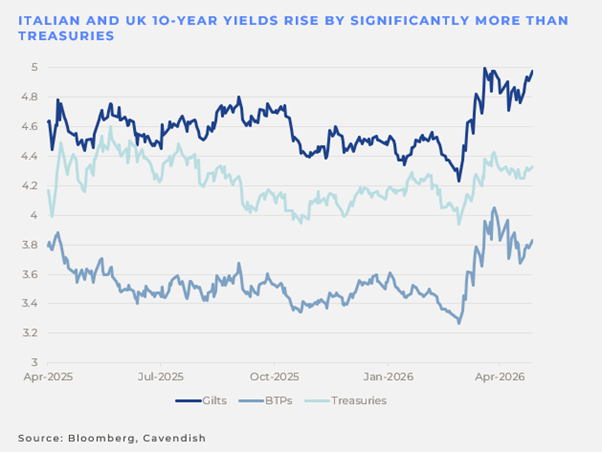

If Starmer does have to step down and a new Prime Minister is appointed, then the UK will have had a staggering eight PMs in the last 20 years, more than in the previous 40 years. Italy, often cited as Europe’s most unstable democracy, had 13 Prime Ministers during their extraordinary political turbulence in the 1970s and 80s.

This is not lost on the bond markets or, sadly, on international investors in the UK as can be seen on the relative borrowing costs of the UK versus the US and Italy.

The question international investors are not unreasonably asking is: has the UK - home of the ’Mother of Parliaments’ - become ungovernable…?

Au revior, Viktor Orban; Bonjour, Rumen Radvev

Just a week after Viktor Orbán was decisively beaten in Hungary’s general elections and the EU lost one ‘thorn in their side’, Rumen Radev won an equally decisive victory in Bulgaria’s general election.

Radev’s pro-Russian stances, including his criticism of military support for Ukraine, have justifiably ruffled some European feathers – will he replace Orbán as the EU’s new eastern thorn?

Some commentators suggest that he will soften his positions for the sake of international relations, much as we have seen Giorgia Meloni collaborate with the EU despite her well-publicised criticisms. But then again Orbán also initially promised to work within the bloc…

Orbán, and now Radev, whilst representing relatively small countries in the EU, highlight a structural vulnerability that the bloc has faced since its inception.

With 27 member states, elections are constant; political churn is inevitable, and consensus on critical issues - from defence to sanctions - is not just a difficult challenge, but one which is constantly shifting. Europe has the resources to counter Russian aggression, but it cannot do so without a strong unified strategy. Celebrating Orbán’s departure risks ignoring the structure that allowed him to become so relatively powerful in the first place… And it’s not just defence.

The same structural weaknesses are visible in Europe’s faltering economic competitiveness. While the recent relaxation of M&A rules for large companies is a step in the right direction, Brussels, as was reported this month by the European Policy Innovation Council, is yet to implement around 90% of the recommendations in the Draghi Report – Mario Draghi’s much discussed blueprint for restoring European competitiveness – despite widespread recognition that they are necessary. For instance, one of the recommendations - combating high energy costs - seems particularly pertinent at present.

Competitiveness depends not just on good policy, but on speed, predictability and the ability to act en masse.

How the EU can respect the preferences of individual member states while implementing policy at a supranational level remains an unresolved tension at the heart of the Union.

Europe’s problem is not that it sometimes chooses the wrong policies; it is that too often it cannot implement the right ones quickly or cohesively enough.

- With thanks to Ioan Peake-Jones

Things to watch...

As seen on Friday 17 April when there were reports that the Strait was opening, the market reaction was profound with the oil price falling almost $10/bbl in an instant. So clearly any re-opening of the Strait as part of the ongoing negotiations would have a significant impact on the market.

As several of the Mag-7 report over the next few days, the focus on AI monetisation is likely to return as well as sensitivity to increased capex if the AI arms race continues.

Central bank meetings will always be closely watched. Whilst there are no rate moves expected, how the respective central banks see the oil spike influencing policy going forward will probably be a key factor in relative market performance.

Roger Lee

Head of Equity Strategy

*This commentary is provided for information purposes only. It does not constitute investment advice or a recommendation. For professional clients only. Views as at the date of publication. No reliance should be placed on this material; onward distribution is the responsibility of the recipient.

Your contact persons

If you have any questions and would like to discuss the topics mentioned in the context of your company, please contact us. We would be pleased to discuss these matters with you, both in Switzerland and internationally, including broader economic topics and global market developments.

Partner

Kurzprofil

Partner

View profile

Partner

Kurzprofil