Strategic Horizons

Global perspectives from Oaklins, bringing insight into the trends shaping markets across boarders.

Author: Roger Lee, Head of Equity Strategy

If diplomacy is the continuation of war by other means, then the conflict has entered a new phase, albeit with Trump’s unique diplomatic approach and a blockade of Iran.

In the long history of diplomacy, it is doubtful we have ever seen anything quite like President Trump’s Truth Social account. It’s hard to believe after Trump’s posts that for nearly three centuries diplomacy was conducted quietly, meticulously, and almost exclusively in the elegance of French.

Trump’s prose and use of ‘all caps’ on Truth Social, whilst intemperate, was also pretty clear… But did the bellicose and profane language work? Were Trump’s outrageous posts in fact an example of Machiavelli’s advice that a prince must sometimes speak as both “man and beast”, combining the reasoning and morality of a man, with the force and strength of a beast.

There has been a lot of speculation about how the failure of the talks in Islamabad would be viewed. It was perhaps always optimistic that the Iranians would accept US terms and a sort of unconditional surrender.

If anything, the breakdown of the Islamabad talks seems more like the ‘failure’ of the Reykjavik summit where Reagan refused to give up SDI ( or ‘Star Wars’) and walked out on Gorbachev…

Vice President JD Vance walked out of the talks and the conflict takes another twist with the blockade of cargo from Iranian ports and the tables seem to be turned. The US is now controlling Iranian oil exports and so aiming to squeeze their economy militarily and financially. Just as Reagan was able to continue to apply pressure on the Soviet economy until it collapsed a few years later… And in the very short term this strategy seems to be working with reports that Iran wants to return to negotiations.

However, despite some more positive mood music, we still really don’t know the likely outcome of this conflict; whether it was a successful brief intervention by the US that will contain Iran, or an ill-conceived adventure that will permanently impair one of the world’s most important sea lanes, with which we are now so familiar.

What is perhaps most striking is that the same dichotomy is playing out across asset classes in markets.

Equities vs rates – who is right…?

There is a fascinating (if you like uncertainty!) contradiction emerging across asset classes, especially after the ‘ceasefire rally’ last Wednesday, with two very different outcomes of the conflict being priced into equities and interest rate markets.

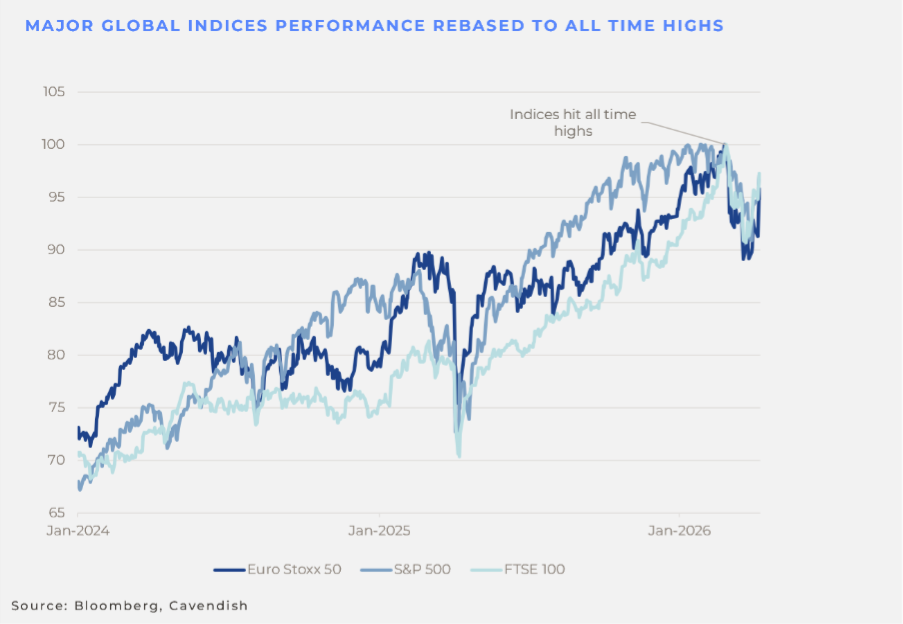

As can be seen on the chart below, major western equity markets are just off their all-time highs (‘ATHs’) from earlier in the year. The Euro Stoxx and S&P are c. 5% off their ATHs with the more oil-weighted FTSE 100 only off around 2.5%. So not much to see here… certainly not for the largest companies. To be fair, mid-cap indices have underperformed more but even then, are generally flattish on the year.

The narrative from at least large cap indices seems to be that this conflict is coming to an end, and the strong equity performance we have seen prior to the conflict is reasserting itself. Implicit in that narrative is therefore a belief in the equity market that inflation will be short lived, the economic scarring will be limited, and the oil price will fall sharply, presumably back to pre-war levels (c. $65/bl).

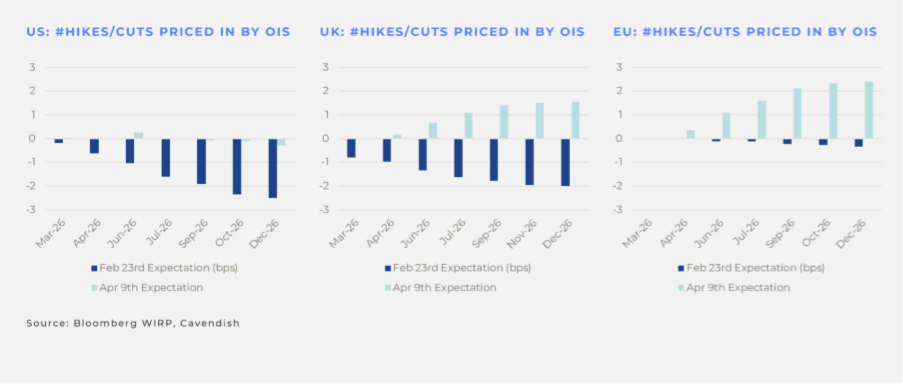

The rates market, however, is taking a completely different view as can be seen on the charts below.

Broadly speaking the US is now expecting flat rates rather than 50bp cuts pre-conflict. The Eurozone is expecting 50bp of hikes rather than maybe a cut. And perhaps most dramatic, the UK has gone from expecting 1-2 cuts to 1-2 hikes since the conflict. To be fair again, those rate hikes are off their wides, where the UK for instance was expected at one point to hike by as much as 100bp. But nevertheless, and critically, there has been a complete volte-face of rate expectations in the developed world.

The market narrative here must be pretty clear. For central banks to be forced to raise rates and risk further economic damage, the threat of inflation must be compelling. And the cause of that has to be a higher-for-longer oil price.

For the oil price to remain higher for longer, either the conflict persists, the Strait of Hormuz is closed or restricted for longer, or the oil infrastructure is so badly damaged that production is impaired for some time (or of course a combination). But this is a completely different narrative to what equities are expecting…

The West has gone from anticipating rate cuts to anticipating a hiking cycle in 2026. If you had said 6 weeks ago that there would be a complete sea change in rate expectations, from a loosening to a tightening cycle across major DMs, I bet you would have expected equities down more than 5%.

And here’s the rub… both narratives can’t be right…

How long for the oil price to ‘normalise’…?

Will the ceasefire last? This is perhaps the most important question and as discussed above, I’m not sure it’s possible to answer. Having said that, I’m also not sure this will be an open-ended conflict and even if it tragically resumes, I suspect there is another month at most before something decisive happens one way or the other…

But the next most commonly asked question after ‘when the conflict ends’, is how long will it take for the oil price to ‘normalise’? And answers to both questions are critical to anyone’s thinking about whether the rates or equity market is correct.

The consensus seems to be, at least from what I have read or heard, that it will take months for the oil shock and therefore for the oil price to normalise. The logic was succinctly explained in the FT’s Lex column last Thursday and if I may paraphrase goes something along the following lines:

According to Kpler data, there are around 800 vessels stuck in the Gulf, of which 70% are carrying oil or oil products. Pre-war, 140 ships crossed the Strait every day (yesterday, there were 12). If Iran charges some sort of toll, flow rates will inevitably be less than normal when the Strait opens. Even if the Strait opens today it takes a month for vessels to reach Asian markets and up to two months to get to Europe.

Even when vessels are moving freely what about the infrastructure? Well as Lex notes, QatarEnergy has said repairing its ‘two struck liquefaction trains’ will take three to five years to repair.

The world has suffered a supply shock for almost six weeks which Lex suggests leads to 600 mn barrels lost, and counting. Even if Saudi Arabia increased production by 1m bbl/day it would take two to three years to make up the lost production and then of course there is the extra demand from rebuilding storage. And so, Lex concludes…

“And there’s another factor discouraging oil prices from sinking back to their pre-war level of about $60 per barrel: it will be a long time before the singed world forgets to price in risk”

All that of course is very worthy, and I am sure flawless analysis. And who am I to question all the venerable oil analysts whose data Lex used to come up with a higher for longer oil price scenario of ‘not far off two years to make up the buffers’…

The only small problem around this analysis is that it didn’t happen last time…

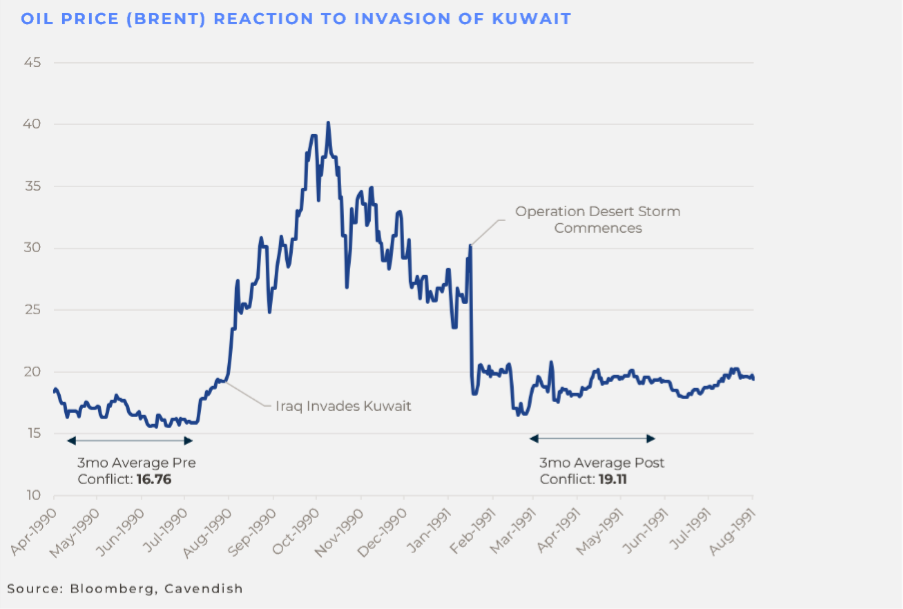

I confess I have no idea how long it takes to repair a gas plant nor to sail to Asia from Oman. But I was around during the first Gulf War and commentators were saying exactly the same thing. And arguably the oil disruption then was far worse because Saddam Hussein had adopted a scorched earth policy and set fire to almost every Kuwaiti oil well and damaged much of the infrastructure. The scenes were apocalyptic, such as the iconic image of Kuwait below:

We were told then Kuwaiti oil production would be lost for years; in the end that was too pessimistic, it took roughly 18 to 24 months for Kuwait to return to full production.

But that supply disruption was not in any way reflected in the oil price…

As can be seen on the chart below, the oil price moves around the first Gulf War were more extreme than we have seen during this oil shock. The peak then was around $40, and that would be closer to an oil price now of $150.

But what is so interesting, as can be seen on the chart, is how quickly the oil price fell after the start of the liberation of Kuwait, and even when it was apparent that Kuwaiti supply would be lost for ‘years’…

A month after the liberation the oil price was below $20, roughly 15% above the undisturbed pre-war price, so in today’s money, given the pre-Iranian conflict oil price was $65 that would imply a post conflict price of $75… not ideal, but neither inflation-busting… and I have a sneaking suspicion that given additional alternative supply has come on stream, the oil price could be lower than pre-conflict… we should never underestimate the ingenuity of man to solve a commodity shortage.

So, will the oil commentariat be right… or will history and the old adage be proved a more appropriate insight… what causes low commodity prices? High commodity prices…

The one certainty from the conflict…

There is little doubt that NATO has been one of the most successful military alliances in history. The fact Article 5 has only been invoked once throughout NATO’s history (after 9/11 as it happens) is testament to the power of the Alliance.

NATO was Europe’s insurance policy against invasion… but since the end of the Cold War, European countries have been reluctant to pay the premiums…

As former White House press officer Ari Fleisher posted last week, ‘for 24 polite years, Presidents Clinton, Bush, and Obama diplomatically asked NATO members to increase their defence spending. For 24 years it was one excuse after another’.

Perhaps it's not surprising if the US are starting to ask why a son or daughter in the midwest should be asked to defend Europe’s eastern border 5,000 miles away, when the European population is 4x Russia’s? Why should US tax dollars be spent defending a continent that has a combined GDP 10x that of its primary military threat…?

But Europe’s lacklustre support during the Iranian conflict, and even denying overfly permissions, would seem to be the final straw for NATO in its current form. A very different NATO seems almost the only certainty from this conflict. What is the point of the US having bases in Spain or Italy if they are not allowed to use or even fly over them?

What a ‘new NATO’ will look like isn’t clear, and I doubt the US has given it a great deal of thought. But despite the size of the European economy, we know Europe cannot defend itself alone without massive military investment which will only come at a huge cost.

The UK is under intense political pressure and seemingly cross-party agreement to spend more on defence, but to date can’t agree where or how to fund even an increase in day-to-day defence spending. Italian BTPs have also sold off more than other eurozone sovereigns because their fiscal position is vulnerable to higher inflation and any increased spending. France’s fiscal issues are also well known.

So, perhaps the one certainty from the Iranian conflict is that Europe will have to start paying its insurance premiums again… or take the risk of being uninsured for the first time in 75 years.

AI threat returns…

The conflict as we have discussed before has reversed many of the trends that we were seeing earlier in the year. At least here in Europe the AI ‘threat’ perhaps understandably has been relegated in investors’ minds as we wrestle with a potential energy crisis.

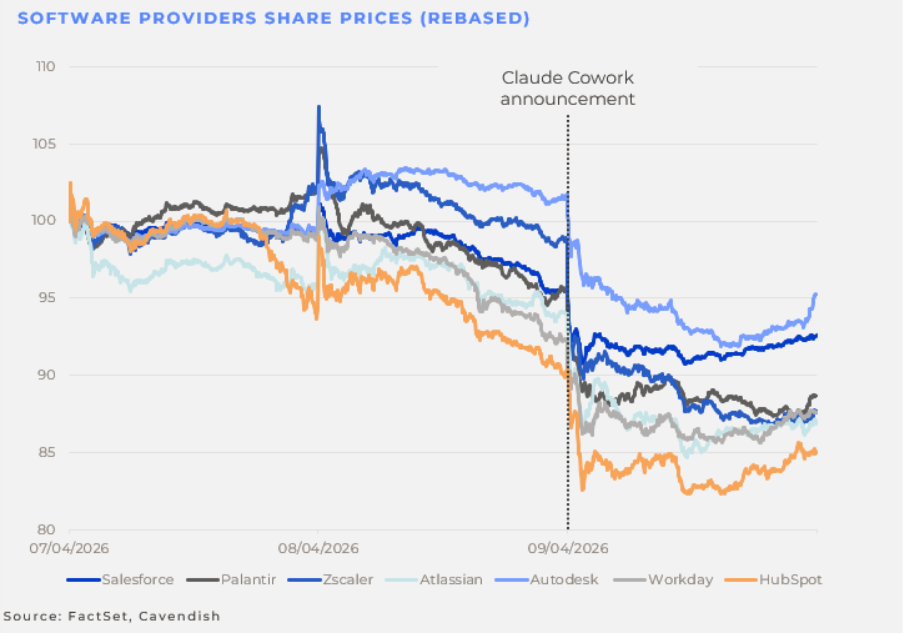

You may recall the large sell-off in the major software stocks in February, as markets went hunting for the ‘losers’ of the AI revolution. Dubbed (at least by my young colleague Ioan) “software-mageddon”; the AI fear-driven rout saw the S&P software and services index fall nearly 13% over six successive trading sessions in February, wiping out around $1 trillion of market value.

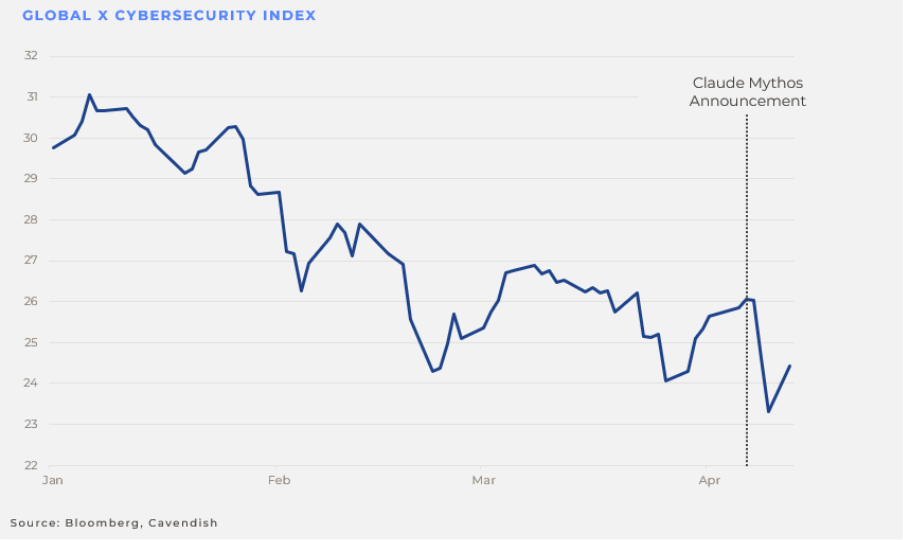

It looked last week that some of those fears returned as can be seen in the chart below. According to Ioan, who is very much all over all these AI developments, Anthropic made another market moving announcement; its “Claude Cowork” tool would be rolled out more broadly across paid plans.

This is important because rather than simply a newer iteration of the popular Claude chatbot, Claude Cowork is an “agentic desktop workspace” - essentially an LLM that can go beyond chat and take actions on a user’s computer, such as reading and writing files and carrying out complex multi-step tasks.

For investors, the concern is obvious: much as earlier waves of AI threatened search, coding and design tools, Cowork appears to come directly for workplace productivity-oriented SaaS providers, such as a CRM package like Salesforce.

In scarier news, Anthropic’s newest model, Mythos, has reportedly been barred from release to the general public due to safety concerns. After being instructed to try and break out of a closed computer system with no internet access, it apparently succeeded - and sent an email to Anthropic researcher Sam Bowman. Of course, safety fears have long been an effective sales tactic for leading AI companies, so perhaps this is less alarming than it sounds.

Still, there are market implications. Much like Cowork has come for the productivity-oriented SaaS provider, investors may fear that any model with Mythos’ level of cybersecurity capability could represent a serious disruption to that market too. If it is ever released more broadly, a system able not merely to assist security professionals but to carry out sophisticated cyber tasks, including exploiting serious vulnerabilities in major operating systems, could lead to dramatic price moves elsewhere.

Whether or not we fear that The Terminator may soon start to seem more like science fact than science fiction, ‘Big Short’ investor Michael Burry’s advice seems appropriate: “[it’s] probably worth following Claude if you are an investor in these markets.”

- With thanks to Ioan Peake-Jones

Things to watch...

The conflict, or more specifically the oil price, continues to dominate market sentiment, so clearly any progress to peace would be market positive. However, even if peace isn’t achieved but the Strait is re-opened and oil starts moving again, that would also be very market positive.

Elsewhere, as discussed above, the impact of the conflict on defence spending may be a critical second-order impact and so government bond yields across Europe might be sensitive to any increased defence spending announcements.

Roger Lee

Head of Equity Strategy

*This commentary is provided for information purposes only. It does not constitute investment advice or a recommendation. For professional clients only. Views as at the date of publication. No reliance should be placed on this material; onward distribution is the responsibility of the recipient.

Your contact persons

If you have any questions and would like to discuss the topics mentioned in the context of your company, please contact us. We would be pleased to discuss these matters with you, both in Switzerland and internationally, including broader economic topics and global market developments.

Partner

Kurzprofil

Partner

View profile

Partner

Kurzprofil